Abbott Laboratories

ABT

is well poised for growth in the coming months, backed by continued robust organic sales increase across each of its operating segments. Further, the raised 2021 outlook is encouraging. However, downsides may arise from foreign exchange headwinds and a challenging business environment.

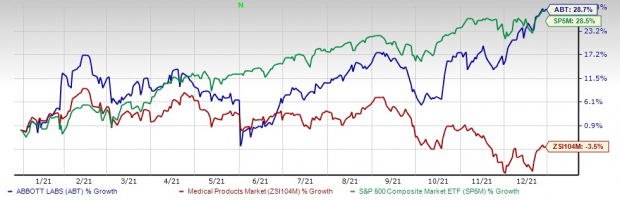

In the past year, shares of this Zacks Rank #2 (Buy) company have gained 28.7% against the

industry

’s 3.5% fall. The S&P 500 rose 28.6% during the same period.

The renowned provider of a diversified line of healthcare products has a market capitalization of $221.16 billion. The company projects 12% growth for the next five years and expects to maintain strong segmental performance. Further, it surpassed estimates in three of the trailing four quarters and missed in one, delivering a surprise of 18.47%, on average.

Riding on current business growth and bullish near-term prospects, the company is worth investing in for now.

Key Growth Drivers

Impressive Q3 Results:

Abbott reported better-than-expected earnings and revenue numbers in the third quarter of 2021. Overall, year-over-year improvements were robust. Excluding COVID-19 testing-related sales, which totaled $1.9 billion in the quarter, organic sales increased 12% year over year. A major point of encouragement, even though COVID-19 case rates surged in the United States and other regions during the third quarter, the company registered strong growth in its more consumer-facing businesses like nutrition, established pharmaceuticals and diabetes care. This mitigated the modest impacts of the pandemic that Abbott witnessed from the surge in cases in certain areas of its hospital-based businesses.

1-Year Price Performance

Image Source: Zacks Investment Research

Diagnostics Grows Amid Pandemic:

Diagnostics sales increased more than 45% (up 12.5% excluding COVID-19 testing-related sales) in the third quarter. With the spike in Delta variant cases, particularly in the United States, demand for testing increased significantly, most notably for rapid tests. In the third quarter, the company sold more than 225 million COVID-19 tests globally and shipped more than 1 billion tests since the pandemic’s start. Over the past several months, Abbott has established a global leadership position in rapid testing, including a supply capacity of more than 100 million tests per month.

Raised Guidance:

Abbott raised its 2021 adjusted earnings per share guidance. Full-year adjusted earnings from continuing operations (excluding specified items of $1.45 per share) are now expected in the range of $5.00- $5.10 per share (compared with the earlier band of $4.30- $4.50).

Downsides

On the flip side, some factors have been deterring the stock’s rally of late.

Foreign Exchange Translation Impacts Sales:

Foreign exchange is a major headwind for Abbott as a considerable percentage of its revenues comes from outside the United States. The strengthening of the euro and some other developed market currencies has been hampering the company’s performance in the international markets.

Tension in China Continues:

Abbott, though it is trying to expand its nutrition business in emerging markets, is facing weakness in Greater China on challenging market dynamics. Especially in pediatric nutrition, the company is apprehensive about the new food safety regulations and a consequent oversupply of products in the market.

Estimate Trends

Abbott is witnessing a positive estimate revision trend for 2021 (ending Dec 31). In the past 90 days, the Zacks Consensus Estimate for its earnings has moved 14.3% north to $5.05.

The Zacks Consensus Estimate for 2021 revenues is pegged at $42.07 billion, suggesting 21.6% growth from the year-ago quarter’s reported number.

Other Key Picks

A few other stocks in the broader medical space the investors can consider are

Apollo Endosurgery, Inc.

APEN

,

Cerner Corporation

CERN

and

West Pharmaceutical Services, Inc.

WST

, each carrying a Zacks Rank #2. You can see

the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Apollo Endosurgery has a long-term earnings growth rate of 7%. The company‘s earnings surpassed estimates in the trailing four quarters, delivering a surprise of 25.6%, on average.

Apollo Endosurgery has outperformed its industry over the past year. APEN has gained 129.1% compared with the industry’s 11.1% growth.

Cerner has a long-term earnings growth rate of 13.3%. The company’s earnings surpassed estimates in the trailing three of the trailing four quarters and met the same in one, delivering a surprise of 3.2%, on average.

Cerner has outperformed its industry over the past year. CERN has gained 18.8% against the industry’s 39.3% decline.

West Pharmaceutical has a long-term earnings growth rate of 27.6%. The company’s earnings surpassed estimates in the trailing four quarters, delivering a surprise of 29.4%, on average.

West Pharmaceutical has outperformed its industry over the past year. WST has rallied 65.2% compared with the industry’s 16.2% rise.

Zacks Top 10 Stocks for 2022

In addition to the investment ideas discussed above, would you like to know about our 10 top picks for the entirety of 2022?

From inception in 2012 through November, the

Zacks Top 10 Stocks

gained an impressive +962.5% versus the S&P 500’s +329.4%. Now our Director of Research is combing through 4,000 companies covered by the Zacks Rank to handpick the best 10 tickers to buy and hold. Don’t miss your chance to get in on these stocks when they’re released on January 3.

Be First To New Top 10 Stocks >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report